|

|

29.03.2017, 01:16

29.03.2017, 01:16

|

#1 |

|

Участник

|

dynamicsax-fico: Parallel inventory valuation – an alternative approach (Part 3)

Источник: https://dynamicsax-fico.com/2017/03/...proach-part-3/

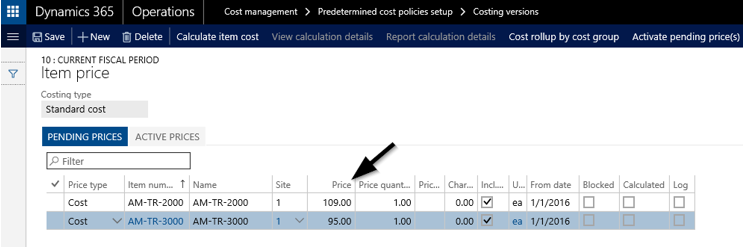

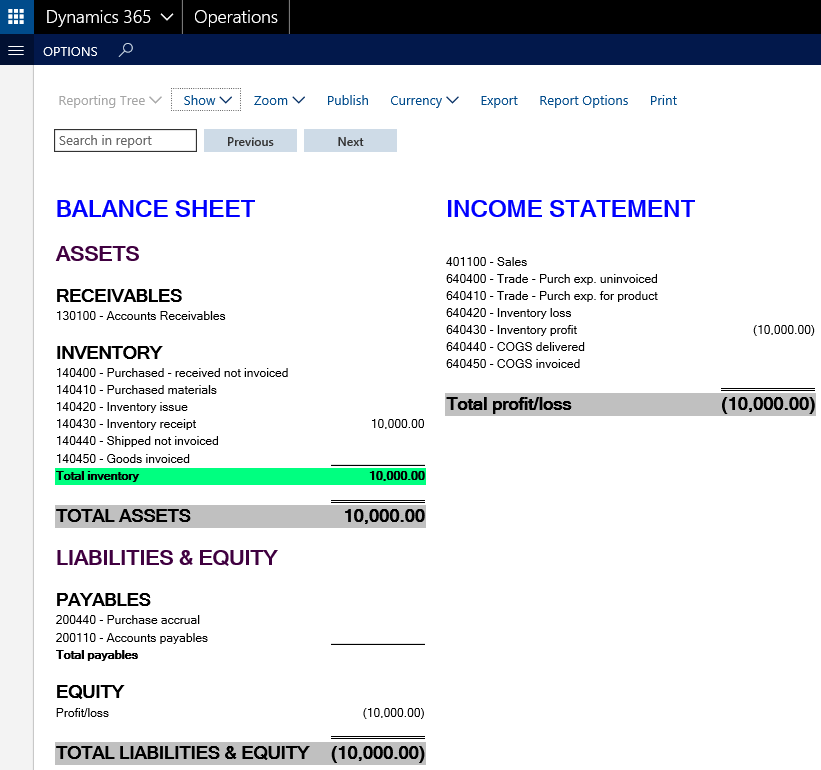

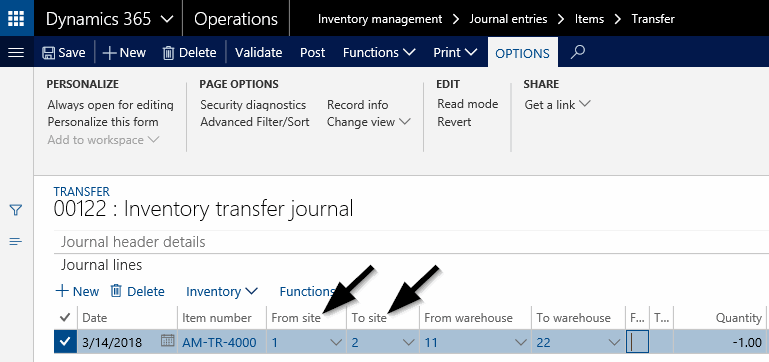

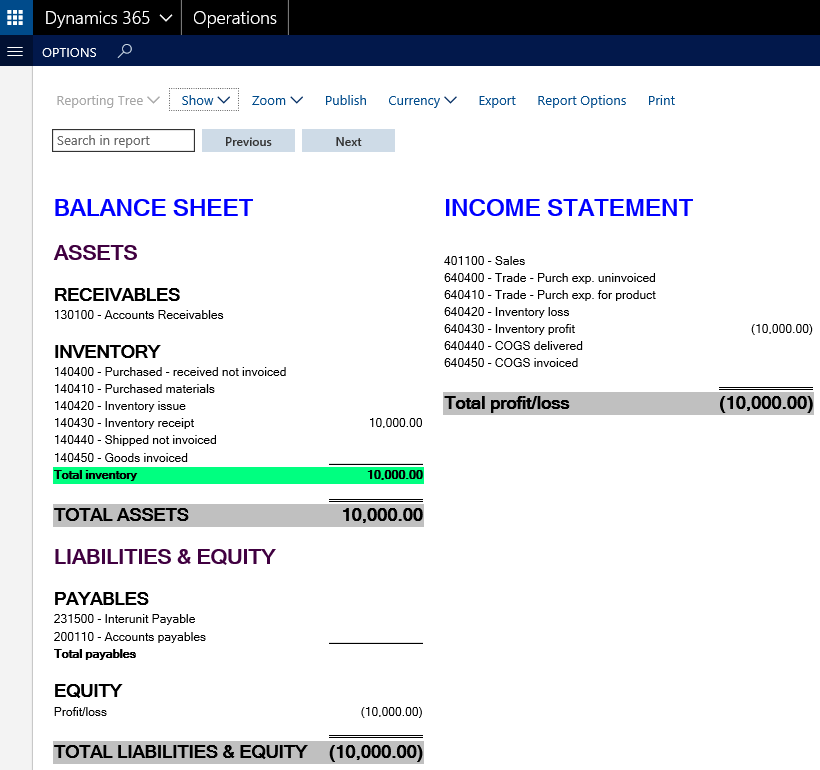

============== The next standard cost variance type that has an influence on the parallel valuation approach concerns cost change variances, which can result from two different sources that will be explained in the following. Source 1: Standard cost price differences between sites Standard costs can be setup in a way that different standard cost prices are defined per site in order to incorporate cost price differences resulting for example from transportation costs, etc. The next screen print exemplifies an item that has different cost prices setup for site 1 and site 2.  In order to illustrate what influence these different cost prices have on the parallel inventory valuation approach, 100 pcs of the item have initially been acquired through an inventory adjustment journal for site 1. The resulting financial data can be identified in the following screen print.  After the items have been acquired, an inventory transfer from site 1 to site 2 for a single item is posted through an inventory transfer journal.  The outcome of this transfer is an adjustment voucher that results in a corresponding increase in the inventory value. The adjustment voucher and the resulting inventory value increase can be identified in the following figures.   What one can identify from the financial statement reports exemplified above is that the total inventory value increased by $25 because of the item transfer from site 1 to site 2. Before analyzing how to deal with that variance for the parallel inventory valuation approach, let’s have a look at the second possible source of cost change variances. Source 2: Customer item return after standard cost price change A second possible source for cost change variances are situations where standard cost items are sold to customers and returned after a cost price adjustment has been completed. The following example illustrates this scenario where initially 100 pcs of a standard cost item with a cost price of $100/pcs are acquired – for reasons of simplicity – through an inventory adjustment journal. The next screen print shows the resulting financial statements.  After the items have been acquired, 5 pcs are sold for a sales price of $200/pcs. With a standard cost price of $100/pcs, the company’s inventory value is consequently reduced by $500, which can be identified from the next financial statement illustration.  Shortly after the items have been sold, the standard cost price of the remaining inventory items is adjusted from $100 to $130. The resulting accounting voucher and financial statements are shown in the next screen prints.   The screen prints above illustrate that the change in the standard cost price resulted in a $2850 higher inventory value [95 pieces x ($130-$100)]. After the standard cost price has been increased from $100 to $130, the customer decided to return 3 out of the 5 pcs sold. Posting the return order packing slip and invoice results in a number of transaction vouchers that are summarized in the next accounting-like overview.   The grey highlighted lines offset each other and can thus be ignored for the analysis of the production costs. The grey highlighted lines offset each other and can thus be ignored for the analysis of the production costs.The transaction vouchers summarized above demonstrate that the item return resulted in a corresponding adjustment of the sales revenue and the receivables amount (3 pcs x $200 sales price / pcs = $600). At the same time, an adjustment of the COGS and inventory value was recorded. Yet, because of the cost price change, a $90 higher inventory value remains. Expressed differently, selling and returning the 3 items resulted in a $90 higher inventory value, which can be identified in the following financial statement overview.  After having analyzed the sources of cost change variances, the question arises, how to deal with them in order to arrive at a parallel actual cost based inventory value? As mentioned in the previous post, standard cost price changes resp. differences typically do not reflect actual (market) price differences but rather cost/transportation/handling cost differences. Moreover, in an actual inventory costing environment, internal movements of goods between different sites do not affect the company’s profit. That is, a company does not get richer or poorer by the mere fact that an item has been shifted from one location to the other, as it might be the case for standard cost items. The same holds for the second source of the identified cost price changes; i.e. in an actual costing environment, a company does not get richer or poorer by shipping and returning goods to and from a customer, as it might be the case in a standard cost environment. For those reasons and because cost change variances affect receipt transactions only, it can be argued that the complete cost change variance amount needs to be shifted from the company’s income statement to it’s balance sheet in order to arrive at an approximate actual cost valuation. This shifting can once again be realized by making use on an allocation rule similar to the one that has been introduced in the prior posts. The next posts will deal with the production related standard cost variances and how to incorporate them in the parallel inventory valuation approach. Till then. Filed under: General Ledger, Inventory Tagged: cost change variance, Inventory, parallel, standard costs, valuation         Источник: https://dynamicsax-fico.com/2017/03/...proach-part-3/

__________________

Расскажите о новых и интересных блогах по Microsoft Dynamics, напишите личное сообщение администратору. |

|

|

|

|

| Опции темы | Поиск в этой теме |

| Опции просмотра | |

|

Комбинированный вид

Комбинированный вид